Income tax planning can add to your future net worth and your future income streams. Here is a line by line view of some of the things that good income tax planning can do to improve your financial life.

Line 10 on your new 1040 return shows your taxable income after all deductions. Knowing your marginal income tax rate is the first step to efficient income tax planning. Lowering your income taxes in the current tax year is not always the best long-term strategy, lowering your lifetime income tax liability is often much more important.

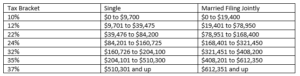

It is important to remember that the current income tax rates for individuals are scheduled to revert to the pre Tax Cuts and Jobs Act rates in 2025. Barring tax changes passed by Congress in the interim, you have six years to utilize the current brackets to your benefit.

Managing Your Income Tax Bracket

Depending on your income level, managing the income tax bracket you fall in may mean realizing extra income to take advantage of a favorable rate; or you may want to lower your taxable income to qualify for a lower tax bracket or other income tax benefits (such as Obamacare).

In my opinion the 12% bracket is extremely valuable. Married couples can have up to $78,950 of taxable income and pay no more than 12% in federal income taxes. Less than 25% of American households have taxable income above this level and I believe the odds of their marginal income tax rate falling is quite small.

If you are among the many that fall into the 12% rate, you should look for ways to pay taxes on as much income as you can without moving into the 22% bracket. Some of the things you should consider are:

Contribute to a Roth IRA or Roth 401k rather than a Traditional IRA or standard 401k account

- You will not receive a deduction for your contribution, but the money will still grow tax free and future withdrawals from this account can also be tax free.

Convert existing Traditional IRA funds to a Roth IRA

- The conversion process will create additional taxable income. If you plan well, you could take money that is subject to potentially higher future income tax rates and pre-pay those taxes at a very favorable rate today.

Take Withdrawals from an Annuity

- Since the first dollar of withdrawals from a tax-deferred annuity are considered ordinary income, withdrawing those funds when you are subject to a lower income tax rate makes a lot of sense. Even if you are still subject to a penalty period for withdrawals from an annuity, most contracts allow for some penalty-free withdrawals.

Realize Long Term Capital Gains

- Rather than deferring gains on appreciated assets, a single filer can pay 0% on capital gains if their income is $38,600 or less; for joint filers the threshold for the 0% rate is $77,200. Delaying gains makes no sense if your taxable income is within these ranges. And unlike taking capital losses, there is no 30-day period for avoiding the wash sale rule. You can sell this morning and buy this afternoon to recognize a gain.

Higher marginal income tax payers will want to take the opposite approach. They’ll want to defer more income unless they anticipate being in an even higher bracket in future years. High bracket individuals will want to:

- Increase contributions to tax-deferred retirement plans.

- Use no-load annuities in lieu of taxable savings vehicles.

- Consider tax-free municipal bonds rather than taxable bonds and savings accounts.

- Locate tax efficient investments in their taxable investment accounts.

- Utilize tax free accounts such as 529 Plans and Health Savings Accounts for appropriate financial goals.

The absolute worst taxable income numbers are $200,000 for single filers and $250,000 for joint filers; along with $157,500 for single filers and $315,000 for joint filers who own their own business.

The first range, $200,000 single and $250,000 joint subjects a taxpayer to the 3.8% net investment income tax.

The second range for self employed filers of $157,500 for single and $315,000 for joint are the cutoff for the pass-through business income deduction.

Taxpayers at those levels should take aggressive steps to lower their taxable income.

Investment Income

Note that these lines have been subdivided into an A and B column. The column on the left is better than the column on the right for income tax purposes.

Tax-Exempt Interest

On the left you have tax-exempt interest, which is income generated from municipal and state government entities. Municipal bond interest is generally income-tax free, although there are some taxable municipal bonds, and some municipal bond interest is subject to the Alternative Minimum Tax.

Tax-exempt interest is also added to your Adjusted Gross Income (AGI) for purposes of calculating how much of your Social Security benefits are taxed. The higher your marginal income-tax rate, the more valuable tax-exempt interest is. To determine the taxable equivalent yield of a tax-exempt security, you divide the tax-exempt yield by 1 less your marginal income tax rate.

For an investor in the 12% marginal income tax bracket, a municipal bond yielding 2.5% gives them the same after-tax return as a taxable security that yields 2.8% (.025/ (1-.12)). For an investor in the 32% tax bracket the same 2.5% yield from a municipal bond equates to a 3.6% taxable yield.

Qualified Dividends

Again, the column on the left is more valuable than the column on the right. A qualified dividend is a dividend from a company that: a) trades publicly on a US exchange and b) is incorporated in a US possession or c) is eligible for the benefits of a comprehensive income-tax treaty with the US. The advantage to generating qualified dividend income is that these payments are taxed at your capital gains rate, which is generally much lower than the rate on your ordinary income

Dividends from REITs, MLPs, employee stock options, tax-exempt organizations, money market accounts, and shares used for hedging are not eligible for qualified dividend status.

Make sure to also consider the treatment of preferred stock dividends. Although ranked below bondholders in the event of financial difficulty, preferred stock pay yields that are similar to long-term bonds. All taxpayers should consider these securities against table bond holdings for the tax advantages alone.

IRAs, Pensions, and Annuities

Income received from pensions and some annuities are absolute, in that you receive the income and you pay the taxes; however, income from an IRA and certain types of annuities are somewhat discretionary. You can plan the timing and the amount you withdraw to achieve the best income-tax outcome for your personal needs. If you are over 70 ½, you are required to take some distributions from your traditional IRA accounts (required minimum distributions/RMDs), but even then you can take advantage of the Qualified Charitable Distribution rules to lower the amount that is reported to the IRS.

Income derived from variable annuities can be problematic for some. All income from variable annuities is considered ordinary income until you have spent down those assets to your cost basis. At that point, the withdrawals are deemed to be return of principal and are no longer subject to income taxes.

Although we prefer to use IRA to Roth IRA conversions to manage income tax brackets for those in the 12% marginal tax bracket, you can certainly use variable annuities in a similar fashion. If you are in a higher marginal tax bracket, you can also consider exchanging your variable annuity for an immediate annuity. Doing this will change the deemed ordinary income rule to a pro-rata distribution rule, where some of your distribution is considered ordinary income and some of it is considered a return of principal.

Social Security

![]()

Sadly, I have to say I have seen cases where an individual is less than 70 years old, in a 30%+ marginal income-tax bracket, saving money, and still insists on claiming their Social Security benefit. It would be a simple fix to suspend Social Security benefits, reduce their taxable income, and accrue delayed filing credits to their future social security income. Yet some will still continue those benefits because they feel they have paid in all their life and want to see some return on their money. Yes, you could die, but throwing away money paying needless taxes is hard to understand.

Additional Income and Adjustments

Under the old tax rules, alimony was deductible to the payer and taxable to the payee. No more–Congress has managed to shift the income tax burden for alimony payments to what is likely the higher earner with the higher marginal income tax rate. If you are divorcing it is important that the income tax liability of alimony payments be considered in developing an equitable settlement.

Business Income/Loss

Capital Gains and Losses

Rental Real Estate, Royalties, Partnerships, S-Corps, trusts, etc.

Adjustments to Income

Self Employed SEP, SIMPLE, and Qualified Plans

An easy way to reduce your current year income tax liability is to contribute to a retirement plan. IRA contributions are reported on line 32, but if you’re self-employed you can defer taxes on even more money. You can establish a SIMPLE retirement plan before October 31 of the current tax year and defer up to $13,000 ($16,000 if you are over age 50) annually.

A SEP retirement plan allows an even bigger tax deferred contribution of up to $56,000, plus a catch-up contribution of $6,000 if you are over age 50. Another useful benefit is you have until your income tax filing deadline, plus any extension, to establish and fund a SEP for the previous tax year. If you’re a business owner who still needs to reduce your previous years taxable income– this is your chance!

Self Employed Health Insurance Deduction

If you’re self-employed, this is where you get to reduce some of your taxable income for health insurance expenses. If you’re not self-employed and are not covered by an employer health insurance plan, this is motivation for starting a side gig.

For example, the mechanic that works on cars after hours, or maybe the carpenter that does an occasional job on the side. Formalize your business to take advantage of this deduction.

In Conclusion

While this is far from an exhaustive list of ways to reduce your income tax liability both now and in the future, you can see there are opportunities for almost everyone to benefit from income tax planning. Take some additional time to review the tax forms you just filed or see a financial planning professional– there is a lot at stake.